Weak global demand for metals, driven by gloomy global growth forecasts (real estate, smelters), is affecting mining companies‘ financial forecasts, noted Simon Lacoume, global economist at French credit insurer Coface.

According to him, the metallurgical sector is struggling worldwide against the macroeconomic context of stagflation.

As a result, there is some risk of insolvencies in mining, smelters and steel mills.

Global demand for metals

Lacoume recommended that metallurgical companies continue to invest in order to achieve sufficient capacities to meet the challenges of the energy transition.

Coface expects high volatility in commodity prices to continue in 2023, especially in metals.

Going forward, the insurer expects base metal prices (steel, copper, etc.) to continue to fall, as the global economic context faces difficulties.

After the inflationary rise in metals (2021/22), accentuated in the first half of 2022 by the war in Ukraine, most metal prices have fallen from their peak for the year.

According to Coface, this is due to two main factors. On the one hand, the financial markets anticipated a slowdown in global GDP. On the other hand, there have been direct effects of rising interest rates on client sectors, such as the construction sector.

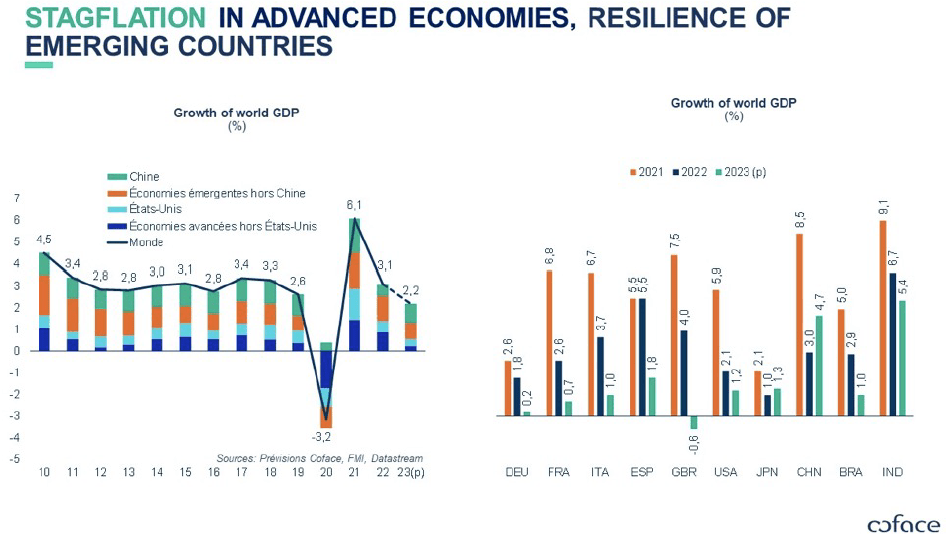

China’s deflating real estate bubble and the slowdown of its economy (4% expected in 2023 compared to 8.1% in 2021) crystallize these concerns.

Consequently, price standardization – relatively close to historical trends – in a global context of inflation (specifically in energy) strongly affects metals producers (e.g. aluminum and steel) and threatens their profitability.

Finally, growing environmental considerations, including compliance with international agreements on the reduction of greenhouse gases, are also pushing some mineral/metal producing countries to stabilize or even reduce their medium-term production targets.

Coface is the world’s third-largest credit insurer, with an estimated market share of 15 percent.