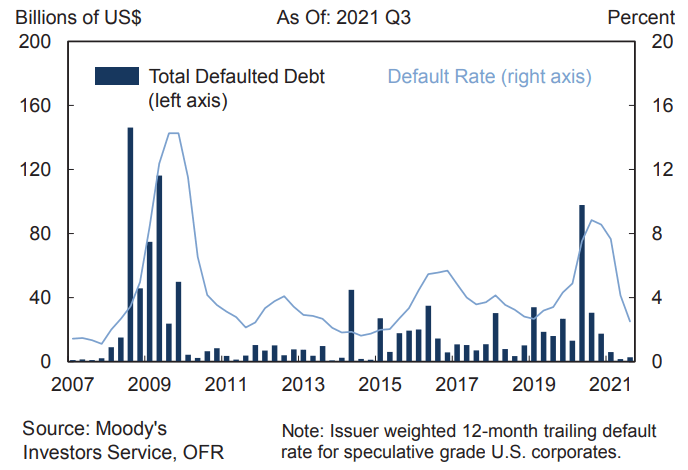

Corporate debt defaults in the United States have fallen sharply, to $10 billion in the first nine months of 2021, the Treasury Department reported.

In 2020, an increasing number of high-yield companies defaulted on their debt obligations, with the default rate for the last four quarters ending in September 2020 reaching a high of 8.8 percent.

While this increase represented the highest default rate in more than ten years, it was well below forecasts made at the start of the pandemic, when all three major ratings agencies projected that the U.S. high-yield corporate default rate it would reach a maximum of between 12 and 15% in early 2021.

US corporate defaults

Since then, according to the Treasury Department, the pace of defaults has slowed considerably, with US corporate defaults totaling just $10 billion in the first nine months of 2021, compared with $159 billion for the entire the year 2020.

Under the most favorable outlook, rating upgrades have outweighed downgrades.

In the last quarters of 202nd and the first three quarters of 2021, the number of upgrades at Moody’s outnumbered downgrades by a record factor of 2.5 to one.

Despite the more optimistic outlook, the Treasury Department said some companies are still struggling to service their debt.

Corporate debt

Additionally, debt levels relative to earnings have remained high for companies in sectors particularly affected by the pandemic, such as airlines, hotels, restaurants and leisure.

However, the high levels of debt in these sectors can be attributed in part to the companies that issue.

Overall, the Treasury Department said that many indicators of corporate balance sheet health have improved since the start of the Covid-19 pandemic.

Low interest rates, coupled with a strong rebound in earnings, helped improve corporate debt service ratios, leverage metrics and overall credit quality.

However, corporate leverage remains high relative to historical standards and companies in sectors particularly affected by the pandemic continue to show strain.

![]()