After performing very well in 2021 and 2022 (due to high freight rates and a rebound in freight demand following the lockouts), shipping lines are expected to see their revenues decline in 2023, projected French credit insurer Coface.

High energy costs and a slowdown in economic activity will reduce freight demand, and therefore freight demand.

This will affect all types of transport (road, rail, air and sea).

In addition, according to Coface, high energy costs will have an effect on the margins of companies in the sector: by increasing production costs and, in the long term, the prices of new vehicles, as manufacturers are forced to pass on part of the increase in production costs in prices.

Shipping lines

On the other hand, ZIM Integrated Shipping Services Ltd. believes that global demand for container shipping is highly volatile in all regions and remains subject to downside risks.

Above all, these risks stem from factors such as reduced consumption, rising interest rates, government-mandated shutdowns and other restrictions from the Covid-19 pandemic still lingering through 2022 (especially in China), severe blows to GDP growth in advanced and developing countries, fiscal fragility in advanced economies, high levels of sovereign debt, highly accommodative macroeconomic policies, and persistent difficulties in accessing credit.

According to a January 2023 International Monetary Fund (IMF) report, global growth is expected to fall to 2.9% in 2023, down from 3.4% in 2022, but to rise to 3.1% in 2024.

Transportation

In line with Coface’s forecasts, air passenger traffic has recovered in most regions following the lifting of mobility restrictions, but has not reached pre-pandemic levels.

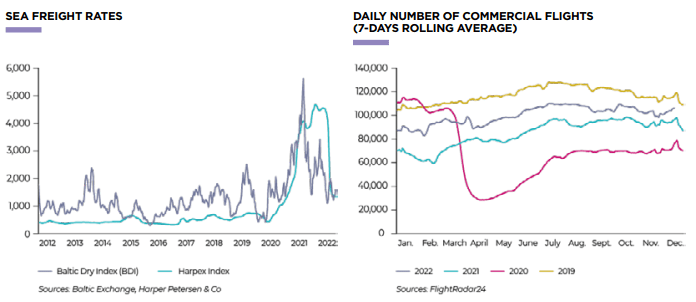

The number of commercial flights in 2022 increased, but remained 10% below 2019 levels.

Aircraft manufacturers Airbus and Boeing have benefited from a strong rebound in orders during the recovery.

However, the global economic slowdown and high energy costs are expected to reduce the number of orders in 2023.

In the longer term, Coface expects the sector to continue to benefit from the need for mobility, the emergence of the middle classes in India and China and cost reductions due to technical advances, particularly in the air and maritime segments.

Environmental concerns and measures to combat greenhouse gas emissions or pollutants could penalize the sector, which is responsible for 23% of CO2 emissions.

However, these concerns could be a boon for vehicle manufacturers, as transport companies are forced to renew their fleets.

![]()