If industrial production in the United States maintains its trend in the third quarter, it could grow by 4.2% annually in 2022, Mexico‘s Ministry of Finance (SHCP) projected.

That rate is close to the median August estimate by private analysts surveyed by Blue Chip of 4.3 percent.

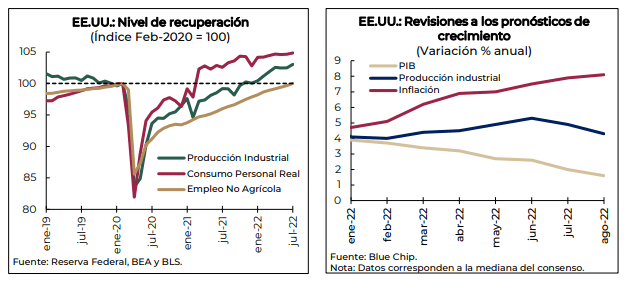

During the first half of the year, the U.S. GDP registered two consecutive quarters of negative growth (0.4 and 0.1%, at a quarterly rate), which generated greater uncertainty regarding the state of economic activity.

In addition to the concern about the technical recession, indicators such as consumer confidence, purchase indices in the services sector and retail sales, showed unfavorable results, or even below what was expected by the analysts’ consensus.

However, the SHCP indicated that other frequent indicators surprised on the upside, suggesting the existence of an economic slowdown, although without strong evidence of a recession.

From their perspective, the good performance of fundamental variables such as private consumption, employment and industrial production provide evidence of this fact, despite the accumulated drop in GDP in the first six months of the year.

For example, industrial production averaged a growth rate of 0.4% per month from January through July 2022.

Particularly in the latter month, production expanded by 0.6% per month in the face of a 0.7% growth in manufacturing, after two months of consecutive declines.

Industrial production

In addition, in August, leading indicators of new manufacturing orders remained in the expansion zone, even above consensus, which shows the resilience of this sector.

Meanwhile, given the lower level of automobile inventories in the United States and the recovery of global value chains, vehicle assembly is expected to continue growing for the remainder of the year, even better than last year.

Other subsectors such as electronics, chemicals and plastics also recorded solid advances during this period, and the same behavior is expected in the coming months.

As for inflation, it continued to accelerate since the second quarter of 2021.

In June 2022 it reached an annual rate of 9.1%, its highest figure observed since 1981, before falling to 8.5% in July.

Inflationary pressures were mainly explained by the contribution of energy and housing rental prices, which in July contributed 2.4 and 1.8 percentage points to the annual variation of the general index in July, respectively.

For the remainder of the year, inflationary pressures are expected to ease in line with a less tight labor market, lower levels of energy prices such as oil and gasoline, and the dissolution of logistical problems that put pressure on global value chains.

![]()