The Mexican government highlighted that it has strengthened the mechanisms for verifying compliance with the VAT-IEPS certification.

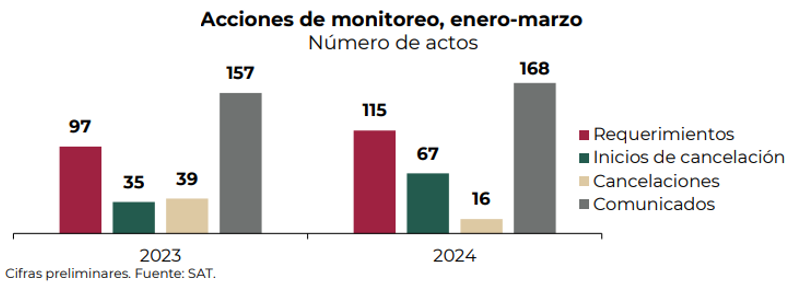

In the first quarter of 2024, the Ministry of Finance and Public Credit (SHCP) conducted 51 compliance monitoring visits.

This figure is 240% higher than the visits made during 2023.

As a result, the requirements or initiation of cancellation proceedings derived from compliance supervision visits and, if applicable, the cancellations resulting from them, have increased with respect to the same period in 2023.

VAT-IEPS Certification

The SHCP also informed that the presumptive balance pending with respect to companies whose registration in the Business Certification Scheme, VAT and IEPS modality, was cancelled was for an amount of 2,179 million pesos.

Thus, with respect to the verification of compliance with the VAT and IEPS Business Certification Scheme (RECE), the monitoring mechanisms were strengthened by prioritizing the authority’s actions focused on removing from the scheme those taxpayers who failed to comply with the requirements for which the certification was authorized, or who improperly use the benefits granted.

The latter is detected through the analysis of the foreign trade operations of the companies registered in the RECE.

Likewise, the SHCP explained that the figure of compliance communications was introduced for those obligations that are easy to correct, mainly the presentation of electronic accounting and compliance opinion, among others.

Mexico’s tax system

Mexico‘s federal tax structure includes both direct taxes, mainly in the form of income taxes, and indirect taxes, mainly in the form of Value Added Tax (VAT) and special taxes, such as the Special Tax on Products and Services (IEPS).

VAT in Mexico has two fixed rates. The first is 8% and is applied in the Northern Border Free Trade Zone. The second is 16% for the rest of the country. In addition, VAT is passed through the manufacturing and distribution chain. Therefore, it is included as part of the final price to the consumer.

On December 30, 2020, a presidential decree was published extending the 8% VAT until 2024. In addition, it also extended the tax credit equivalent to one third of the income tax caused in the Northern Border Free Trade Zone.

Likewise, another decree issued on the same day extended until 2024 the 8% VAT benefit in certain municipalities of the southern border. This decree also includes a tax credit equivalent to one third of the income tax caused in that region.