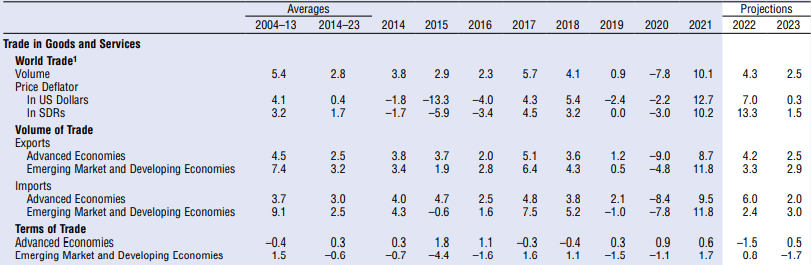

World trade growth is slowing sharply: from 10.1% in 2021 to a projected 4.3% in 2022 and 2.5% in 2023, the International Monetary Fund (IMF) highlighted.

This is higher growth than in 2019, when rising trade barriers constrained global trade, and than during the Covid-19 crisis in 2020, but well below the historical average (4.6% for 2000-21 and 5.4% for 1970-2021).

What is happening? The slowdown, which is 0.7 percentage points sharper than that forecast for 2023 in the July update of the IMF report, mainly reflects the slowdown in global output growth.

Summary of World Trade Volumes and Prices (Annual percent change, unless noted otherwise)

In particular, supply chain constraints have been a further drag: the Federal Reserve Bank of New York‘s Global Supply Chain Pressure Index has declined in recent months-largely due to a slowdown in Chinese supply lead times-but remains above its normal level, indicating continued disruptions.

However, supply chains are complex, and pandemic-era disruptions were the product of multiple factors.

If other factors continue to improve even as challenges in China persist, the IMF forecasts that supply-side pressures may continue to ease.

World trade

The appreciation of the dollar in 2022-about 13% in nominal effective terms in September, compared with the average in 2021-is likely to have further dampened global trade growth, given the dollar’s dominant role in trade invoicing and the implicit pass-through of consumer and producer prices outside the United States, according to the IMF.

While global trade growth is slowing, world trade balances have widened.

After narrowing during 2011-19, global current account balances-the sum of current account surpluses and deficits of all economies in absolute terms-increased during the Covid-19 crisis and are projected to widen further in 2022.

The widening of balances has reflected the impact of the pandemic.

It has also reflected, in 2022, the rise in commodity prices associated with the war in Ukraine, which has raised the balances of net oil exporters and reduced those of net importers.

An increase in global current account balances is not necessarily a negative development, although excessive global imbalances can fuel trade tensions and protectionist measures or increase the risk of disruptive movements of currencies and capital flows.

![]()